Most failed Section 351 exchanges do not fail because the strategy is wrong. They fail because of preventable errors that surface late in the process or, worse, after the transaction has closed. The tax authority is well established. The mechanics are well understood. The errors are usually in the execution.

This guide walks through the most common mistakes we see in Section 351 ETF exchanges and explains how to prevent each one. Some are tax errors. Some are operational errors. Some are documentation errors. All of them are avoidable with the right preparation. Where the right answer depends on your facts, consult your tax advisor before relying on any conclusion here.

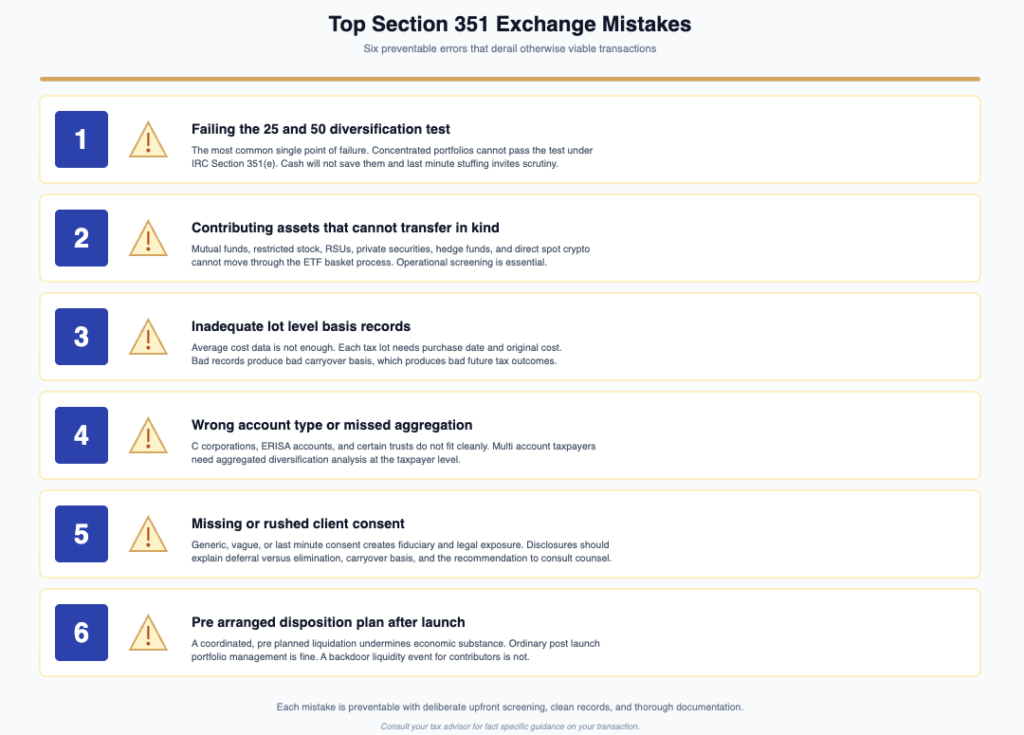

Mistake one. Failing the 25 and 50 diversification test

The single most common mistake is misjudging the diversification of the contributed portfolio. The investment company limitation under IRC Section 351(e) and Treasury Regulation Section 1.351-1(c) requires that the contributed portfolio already be diversified, measured by the 25 and 50 test. No single holding above 25 percent of contributed value, no top five combined above 50 percent.

Several specific traps live inside this rule. Cash and cash items are excluded from the total assets denominator, so adding cash does not dilute concentration. Different share classes of the same issuer must be combined. The look through rule examines the underlying holdings of contributed ETFs, mutual funds, and closed end funds, so a concentrated position wrapped inside an ETF is still concentrated for the test.

The fix is a thorough position level diversification analysis early in the process. If the portfolio fails, the right move is to address the concentration before the contribution rather than try to engineer around the test at the last minute. Last minute purchases of diversifiers, sometimes called stuffing, can invite scrutiny and cause the exchange to fail.

The 25 and 50 test is not a soft guideline. It is a hard requirement under the investment company rules, and the most common single point of failure in a Section 351 exchange.

Mistake two. Contributing assets that cannot be transferred in kind

The second common mistake is treating Section 351 as if it were a pure tax rule. The tax code under IRC Section 351(a) is fairly permissive about what counts as property. The ETF basket process is much narrower.

Mutual fund shares cannot be transferred in kind through the standard ETF process and generally cannot be contributed. Restricted stock and unvested RSUs carry transfer limitations that prevent in kind delivery. Private securities, hedge fund interests, and most alternatives are blocked by structure. Direct spot cryptocurrency cannot enter a standard ETF without specific structural accommodation.

Foreign equities from markets that do not allow in kind creations and redemptions are also blocked. The list of restrictive markets shifts over time, so each foreign holding needs current verification rather than reliance on memory.

The fix is operational screening at the position level before any commitment is made. Every line in the contributed portfolio needs to clear both the tax filter and the operational filter.

Mistake three. Inadequate lot level basis records

The third common mistake is underestimating the basis record requirement. Section 351 generally provides carryover basis treatment, which means the basis of the contributed property attaches to the new ETF shares received. If the basis records are wrong, the tax outcome is wrong.

Average cost basis data is not adequate. Each tax lot needs purchase date and original cost basis recorded individually. This becomes especially difficult for very old positions, positions that have moved between custodians, positions affected by corporate actions, and positions held in accounts that have changed ownership over time.

Custodial records are the primary source, but they are not always complete. A custodian may show clean lot level data for recent purchases but only summary data for older positions. A position transferred from another firm years ago may have arrived with incomplete data and never been corrected.

The fix is to start the basis collection conversation early in the process. Identify the gaps, work with the custodian and prior custodians where needed, and either resolve the records or exclude the affected positions from the contribution.

Mistake four. Wrong account type

The fourth common mistake is attempting to use accounts that do not fit the Section 351 framework. Standard taxable brokerage accounts owned individually, jointly, or through a revocable trust generally fit. Many other account types do not.

C corporations create complications and may introduce a built in gains issue if appreciated assets are later sold inside the structure. ERISA accounts, including most 401(k) plans and certain pension structures, generally cannot transfer assets in kind without a specific Department of Labor exemption. Non grantor trusts, S corporations, and various other structures each carry their own analysis.

The diversification test under IRC Section 351(e) is also typically applied at the taxpayer level rather than the account level. A client with appreciated assets across an individual account, a joint account, and a trust account may need an aggregated review that catches concentration not visible from any single account.

The fix is to confirm account type and ownership structure during initial screening. Anything other than a clean taxable account warrants extra diligence and consult your tax advisor.

Mistake five. Missing or inadequate client consent

The fifth common mistake is treating client consent as a formality. Written consent from each contributor is essential. The consent should explain the basic transaction, the tax deferred nature of the exchange, the carryover basis treatment, the recommendation that each client consult their own tax advisor, and any other material disclosures.

A consent that is too generic, too vague about the tax outcome, or too rushed in the days before closing creates risk. The contributor may not understand what they signed. A future complaint or claim becomes harder to defend.

For advisors specifically, the consent should be paired with a documented process showing how the recommendation was made, why the strategy fits the client, and what alternatives were considered. Fiduciary duties do not pause during a Section 351 exchange.

The fix is a deliberate, well documented consent process that begins well before the closing date. The client should have time to read the disclosures, ask questions, and consult outside counsel if they wish.

Mistake six. Pre arranged sale or disposition plan

The sixth common mistake is having a pre established plan to dispose of the contributed assets immediately after launch. Ordinary portfolio management inside the new fund is fine. A coordinated, pre arranged liquidation program can undermine the economic substance of the exchange and create exposure to challenge.

This issue can surface in subtle ways. A fund sponsor who tells contributors that the contributed positions will be quickly rotated out of the fund. A contributor who is told they can effectively exit specific positions through post launch sales by the fund. A management agreement that contemplates rapid disposition of contributed holdings.

None of these patterns is automatically fatal, but they all increase the risk that the transaction is recharacterized as something other than a clean Section 351 exchange. The cleaner the post launch management is from any pre arranged liquidation plan, the better the position.

The fix is to keep the post launch management discussion separate from the contribution decision. The fund operates under its prospectus. The portfolio manager exercises ordinary judgment. The contributor accepts ETF wrapper exposure rather than a backdoor liquidity event.

Mistake seven. Ignoring affiliated transaction rules

The seventh common mistake, especially relevant for advisors, is overlooking the affiliated transaction analysis. When an advisor or its clients may be affiliated persons of the new fund under Section 17 of the Investment Company Act of 1940, the transaction may need to comply with specific compliance rules including Rule 17a-7.

This is a fact specific compliance question that should be reviewed with counsel. The presence of affiliation does not necessarily prevent the transaction. It does require additional documentation, additional procedural steps, and sometimes board level approvals.

The fix is to surface the affiliation question early in the process and engage qualified counsel. It is a much smaller problem when identified during initial structuring than when discovered close to the closing date.

Mistake eight. Contributing positions with embedded losses

The eighth common mistake is contributing positions that are sitting on losses. Section 351 carries over basis rather than stepping it up. A loss position contributed into the new fund is a loss the contributor can no longer harvest.

The better practice is to harvest losses before contribution analysis begins. The loss harvest produces a current tax benefit. The proceeds can be redeployed into other positions, including positions that may themselves become candidates for contribution.

This mistake is particularly common with portfolios that have a mix of large winners and a few unrealized losers. The instinct to keep the portfolio intact during the contribution process can result in giving up the loss permanently.

The fix is a tax planning conversation that separates the loss harvest decision from the contribution decision. Each one is its own decision and each one deserves its own analysis.

Mistake nine. Misunderstanding what gets deferred

The ninth common mistake is conflating tax deferral with tax elimination. Section 351 defers recognition of gain. It does not erase gain.

The basis of the contributed property carries over into the new ETF shares. Future sales of those shares trigger gain measured against the carryover basis. The character of the gain generally tracks the original holding period.

For long term holders who plan to continue holding the ETF shares, the deferral can be highly valuable. Capital that would otherwise have gone to current taxes continues to compound. For investors who plan to sell soon after the exchange, the benefit is much smaller because the deferred gain comes back into the picture quickly.

The fix is a clear conversation with each contributor about what the strategy actually does and does not do. Misalignment between expectations and reality is a common source of post closing dissatisfaction.

A short prevention checklist

Most of the mistakes above can be prevented by the same basic discipline. Run the diversification analysis early at the position level with look through. Confirm asset eligibility against the in kind transfer requirements. Collect lot level basis records well in advance. Confirm account type and ownership structure. Document client consent thoroughly. Avoid any pre arranged disposition plan. Surface affiliation questions early. Harvest losses before contribution. Set realistic expectations about deferral versus elimination.

When all of these are addressed deliberately, the closing process is generally clean. When they are addressed reactively, problems tend to compound. Consult your tax advisor whenever the answer is unclear in your specific situation.

Frequently asked questions

What is the most common reason a Section 351 exchange fails Diversification failure under the 25 and 50 test is the single most common cause. Concentrated positions, missed share class combinations, and look through analysis on contributed ETFs all show up regularly.

Can a portfolio be fixed if it fails the diversification test Sometimes. Position level changes before the contribution may bring the portfolio into compliance. Last minute additions designed solely to pass the test can invite scrutiny and should be approached with caution. Consult your tax advisor.

What happens if basis records are incomplete Affected positions are typically excluded from the contribution. The contributor either continues to hold those positions outside the fund or pursues a separate cleanup of the records before any future contribution.

Are mutual funds ever workable in a Section 351 contribution Generally no. Individual mutual fund shares cannot be transferred in kind through the standard ETF process. The fix is typically to liquidate mutual fund positions before the contribution analysis begins.

Does a Section 351 exchange create any reporting obligations Yes. The non recognition treatment is reflected in the contributor’s tax return for the year of the exchange, and the carryover basis is recorded on the new ETF shares for future reporting. Consult your tax advisor for the specific reporting in your situation.

How do I know if I have an affiliation issue This is a fact specific compliance question that needs to be reviewed with qualified counsel. The analysis turns on the relationships among the advisor, the fund sponsor, the contributors, and the fund itself.

Conclusion

The mistakes that derail Section 351 exchanges are rarely glamorous. They are documentation gaps, missed diversification math, ineligible account types, late surfacing affiliation issues, and contributors who did not fully understand what they were signing. Each one is preventable with the right discipline applied early in the process.

A successful Section 351 exchange looks boring from the outside. The screening was careful. The records were clean. The consent was thorough. The closing was uneventful. The post launch reporting was straightforward. That is exactly what you want.

The path to that outcome is the prevention checklist above, applied deliberately, with your tax advisor involved at every consequential decision point.