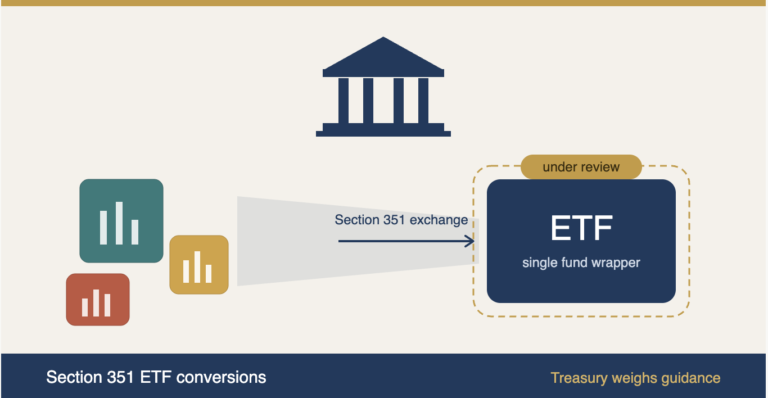

The landscape of Section 351 exchanges continues to evolve as regulators, lawmakers, and market participants respond to the growing use of tax-deferred contribution structures—particularly in the context of ETF conversions. Recent updates from the Internal Revenue Service have placed renewed focus on how continuity-of-interest requirements are applied, signaling a more structured approach to transactions that were previously considered routine.

One of the key developments is the IRS’s emphasis on ensuring that shareholders maintain a meaningful equity stake post-transaction. This clarification is especially relevant for firms pursuing conversions into exchange-traded funds under the Investment Company Act of 1940 framework. As asset managers continue to leverage Section 351 to facilitate tax-efficient restructurings, these interpretations could influence how deals are structured moving forward.

At the same time, policymakers are exploring whether additional legislative guardrails are needed. Discussions in U.S. Congress suggest growing scrutiny around perceived loopholes in tax deferral strategies, particularly when applied at scale. While no sweeping reforms have been enacted yet, the direction of these conversations indicates a potential shift toward tighter compliance expectations in the near future.

From a market perspective, these regulatory signals are already shaping behavior. Asset managers and legal advisors are reassessing transaction timelines, documentation standards, and risk exposure. Firms involved in ETF conversions are paying closer attention to structuring details to ensure alignment with both current guidance and anticipated changes.

For practitioners, staying ahead means more than just monitoring official releases—it requires understanding how guidance, legislation, and market practice intersect. As Section 351 exchanges remain a cornerstone of tax-efficient structuring, the ability to adapt quickly to regulatory nuance will be a defining factor in successful execution.